Stamp Duty has been a topic of discussion this year as chancellor Rishi Sunak introduced a Stamp Duty holiday to encourage the housing market to keep moving during the pandemic. With the holiday now over, homebuyers are having to pay the tax again and figures show the amount being paid has soared.

Stamp Duty was first introduced in 1997 and the amount paid by homebuyers has increased by an average of 8.4% every year, according to the Financial Reporter. The average family buying a home now faces a Stamp Duty bill of £3,548. This compares to £601 paid in 1997.

The increase is due to average house prices soaring. According to Land Registry data, the average house price in January 1997 was £60,698. By January 2021, the average price had risen to £248,946.

If you’re planning to move home, you need to factor in the cost of Stamp Duty or you could end up with an unexpected bill.

What is Stamp Duty?

Stamp Duty is a tax you may have to pay when you’re buying property or land in England or Northern Ireland above a certain price. In Scotland, Land and Buildings Transaction Tax is similar, as is Land Transaction Tax in Wales.

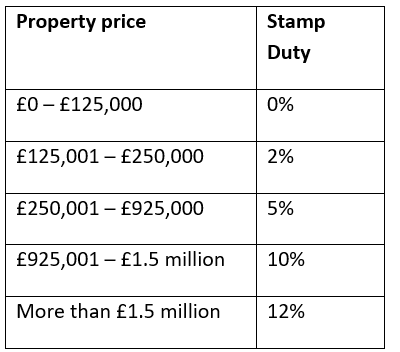

The amount of Stamp Duty you pay is based on how much the property is worth. The tax bands for a property you plan to live in are:

The tax is calculated on the part of the property falling into each tax band. So, if you purchase a property for £300,000, the first £125,000 is not liable for Stamp Duty. You will then pay 2% on £125,000 and 5% on the final £50,000. This leads to a Stamp Duty bill of £5,000 to pay.

If you’ve not accounted for Stamp Duty, you could face an unexpected bill when you move home.

You have up to 14 days after you complete the purchase of your property to file a return to HMRC and pay any Stamp Duty that is due. Your solicitor will usually calculate and pay the Stamp Duty on your behalf. They will usually collect the money due before you complete the purchase to speed up the process.

Even if no Stamp Duty is due, you will still need to complete a return to claim relief.

While the above table applies to most home purchases, there are some exceptions.

The first-time buyer’s relief

If you’re buying your first home, you’ll benefit from a relief before Stamp Duty is due. If you’re buying a home with a partner who has previously owned a property, you won’t get Stamp Duty relief.

First-time buyers don’t have to pay Stamp Duty if the property is valued at less than £300,000. For many first-time buyers, this means they won’t need to consider Stamp Duty. If you’re buying a property that is more than £300,000, you could save up to £5,000 thanks to the relief.

Let’s say you’re a first-time buyer purchasing a property for £500,000. The first £300,000 will be free from tax, while the remaining £200,000 will be liable for 5% Stamp Duty, resulting in a £10,000 tax bill.

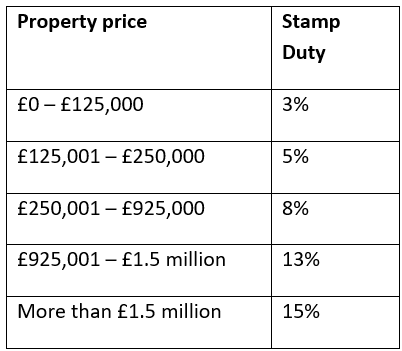

Stamp Duty surcharge for additional properties

When buying a home that you don’t plan to live in, you will need to pay an additional 3% Stamp Duty surcharge. This may include properties you want to purchase as a second home, holiday home, or buy-to-let.

This means the Stamp Duty tax bands for additional properties are:

Overseas buyer surcharge

Since April 2021, overseas-based buyers of residential property in England and Northern Ireland will need to pay an extra 2% on top of the standard Stamp Duty rate. This applies whether you’re buying a home or an additional property. So, if you’re an overseas buyer and want to purchase a holiday home, you’d face a 5% Stamp Duty surcharge – 3% due to it being an additional property, and 2% because you are based overseas.

6 Stamp Duty exemptions

There are also times when no Stamp Duty is due. These include:

- No money or other payment changings hands for a land or property transfer

- The property has been transferred as part of a divorce or dissolution of a civil partnership

- You inherit a property through a will

- You buy a new or assigned lease of seven years or more, as long as the premium is less than £40,000 and the annual rent is less than £1,000

- You use alternative property financial arrangements

- You buy a freehold property for less than £40,000.

If you’re planning to buy a new property, whether a first home or a buy-to-let investment, we’re here to help you secure a mortgage and understand your options.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.