When you retire, your income may be coming from multiple sources, and it may not be regular. This can lead to some retirees being overtaxed. While you can claim back overpaid tax, it could affect your plans and you may not realise you’ve paid too much.

Understanding your tax liability can help you manage your budget and income in retirement.

Retirees have overpaid around £835 million in tax since 2015

In the last quarter of 2021 alone, HMRC returned more than £42 million in overpaid tax to those accessing their pension, according to an FTAdviser report.

Retirees affected, on average, will receive a rebate of £3,107.

Since the government introduced Pension Freedoms in 2015, which allows retirees to access their savings flexibly, HMRC has repaid around £835 million in overpaid tax.

Overpaying tax is common among retirees because of the way the tax system works, and there have been calls for it to be updated to reflect the 2015 pension reforms.

The issue arises if you’ve not been given a tax code by HMRC. This can mean you’re given an emergency tax code that assumes you’ll make the same withdrawal each month.

So, if you withdraw a lump sum from your pension to pay for one-off expenses or to last for several months at the start of the tax year, the system assumes you will do this each month. As a result, you may pay too much tax.

Let’s say you withdraw £20,000 from your pension in April as you want to help your child get on the property ladder by gifting a deposit. The system may tax this withdrawal as though you’re going to withdraw an annual income of £240,000.

So, you could end up paying far too much tax if your initial withdrawal doesn’t accurately reflect the income you’ll take from your pension over the tax year.

How much tax do retirees pay?

To understand if you’ve overpaid tax, you need to start with your tax liability.

First, you can typically take up to 25% of your pension tax-free. You can either take this as a lump sum or spread it out.

For any other withdrawals you make from a defined contribution (DC) pension, you may be liable for Income Tax.

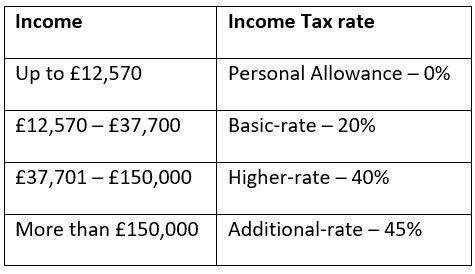

Your retirement income is taxed in the same way as your income was when you were working. The below table shows the 2022/23 Income Tax rates.

Keep in mind that you need to consider all forms of income, not just withdrawals you make from your DC pension. So, if you receive income from a defined benefit (DB) pension, rental properties, or investment portfolio, for example, you could be liable for a higher rate of tax.

In retirement, your income may be complex, and it may come from multiple sources. It can be difficult to keep track of your income and tax liability. We’re here to help you understand what tax you need to pay and how to make use of allowances to make your money go further.

How to reclaim overpaid Income Tax

If you’ve overpaid tax, don’t panic.

If you discover you’ve overpaid tax, you can apply for the money back now and HMRC will return it within 30 days. You will need to fill in a form to apply, which you can do online or through postal forms. Which form you need to complete will depend on your circumstances:

- P55 – If you’ve taken an income from your pension but have not emptied it.

- P50Z – If you have emptied your pension and have no other taxable income in the same tax year.

- P53Z – If you’ve emptied your pension and have other taxable income.

You will need to provide information about how much you withdrew from your pension and the tax you paid. HMRC will then calculate what you’re owed.

Even if you don’t realise you’ve overpaid, you will receive a refund automatically at the end of the tax year. This means you could be waiting almost a full year to get your money back if you don’t spot the error.

While you will receive overpaid tax back, it can be frustrating, and it may affect your plans if it’s not something you’re expecting. Working with us can help you minimise the chance of overpaying Income Tax and mean that you’re aware as soon as possible if it does happen.

If you’d like to discuss your retirement income and how much tax you could pay, please contact us.

Please note: This article is for information only. Please do not act based on anything you might read in this article.

All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate tax planning.